No products in the cart.

Accelerating Value Creation Through Leadership: Putting Hard Numbers on the Soft Stuff

Talent Investments that Make Value Creation Plans Inevitable

In the Marine Corps, before executing a mission, we ran what was called a leader’s reconnaissance (leader’s recon, for short). The team leader got physically close to the objective before committing his Marines to take it. He studied it from every angle, validating with his own eyes what the map and the intelligence briefing had implied. The principle was simple: the most consequential decisions deserve the most rigorous ground truth.

PE deal teams run their own version of a leader’s recon on almost every input to a deal. Market diligence. Commercial diligence. Financial diligence. Data and technology diligence. Legal and tax reviews. The one major input where most firms still operate on relationships and gut feel is the one most likely to determine the outcome: the leaders who will execute the value creation plan.

AlixPartners’ 2025 PE Leadership Survey put it bluntly: effective leadership is the strongest lever for value creation in private equity. With the financial tailwinds of the last decade receding, the team running the company is the input most likely to determine whether the deal performs or not.

Every PE firm we work with now does some form of talent diligence. The question that will define which firms pull ahead in the next cycle isn’t whether you do it; it’s whether you’re doing it in a way that makes the value creation plan inevitable, or whether you’re just checking a box and hoping for a better outcome.

Where Today’s PE Talent Diligence Falls Short

What I would call PE Talent Diligence 101 looks like this: a couple of dinners and meetings with the CEO and maybe a structured interview process for the CFO and a few other key roles like Business Unit Leaders and the Head of Sales. Many PE firms feel this is sufficient because they already believe they selected the right investment. This hubris fails to recognize a mediocre team can destroy an excellent investment, and an excellent team can make a mediocre investment excel. Without any depth or breadth of talent diligence, it is guaranteed to fall short, and there are three typical reasons why.

It Looks Backward and Inward

A structured interview has two limits. First, it can only probe what’s already happened. “Tell me about a time when…” “Walk me through a difficult turnaround.” That works if the future looks like the past. In most PE-backed leadership roles, it doesn’t, because the company is supposed to become something different by the end of the hold period.

Second, the candidate is both subject and source. They control the narrative and whether intentional or not, they remember selectively and insert bias into their experience. Even a rigorous interview can’t fully neutralize the fact that you’re getting one version of events from a source with a vested interest in the outcome.

The canonical meta-analysis in personnel selection (Schmidt and Hunter, 1998) puts the predictive validity of a well-designed structured interview at about 26 percent of who will perform well in a future role. That makes it one of the better single methods in scientific literature, and a genuinely useful input. It also means nearly three-quarters of the picture must come from somewhere else.

As Marshall Goldsmith put it best: what got you here won’t get you there. The leader who got the company to the deal isn’t necessarily the leader who can take it to the exit.

It’s One-Dimensional

Most firms in this space run a structured interview, period. Or a personality assessment, period. Each is useful on its own; neither is sufficient on its own. There’s a well-documented effect in industrial-organizational psychology called leadership emergence, distinct from leadership effectiveness. People who emerge as leaders in a group as tall, articulate, confident, etc. aren’t necessarily the people who turn out to be the most effective in the role. We tend to “fall in love” with those leaders. An interview, even a well-structured one, rewards emergence. A multi-factor approach disentangles the two.

It Stops at a Snapshot

Most assessments end with a verdict: yes, no, maybe. That verdict is the talent equivalent of doing your financial diligence and then taking the seller’s word for financial projections. A snapshot tells you what you have at a particular moment in time. It doesn’t tell you about what you need in the future and what investments you should make in someone’s development to fill in gaps.

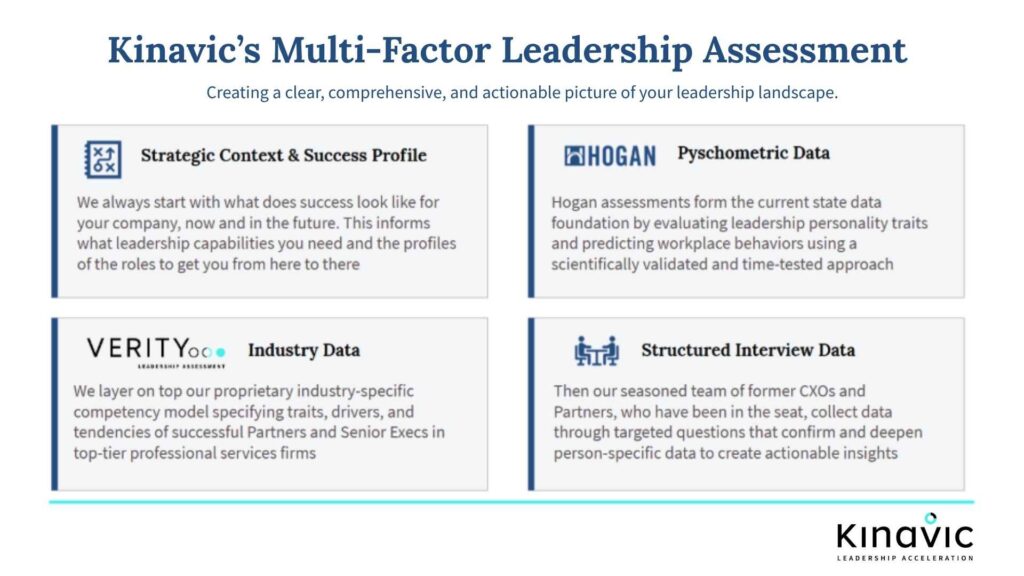

What Right Looks Like: Multi-Factor and Future-Focused

The right approach to talent diligence starts with a leadership success profile, the same construct we developed in our piece on bold leadership in the AI era: the capabilities required to execute this specific VCP, built forward from what the company has to become.

You then assess against that profile using four factors in combination.

Strategic Context & Success Profile built from knowledge of the company and its VCP: strategy, capital structure, culture, market dynamics, the team around the role, and the inflection points where leadership matters most. While assessment data and interviews tell you what kind of leader you have, context tells you what kind of leader the deal needs.

Psychometric data, like Hogan, with criterion validity on par with cognitive ability tests. The highest-value output in PE diligence isn’t measuring strengths (those surface in any interview), it’s measuring derailers: the personality tendencies that emerge under pressure and torpedo otherwise capable leaders.

Industry data that serves as a proprietary success database of what drives outcomes in roles like this one. At Kinavic, we use the Verity Leadership Assessment℠, built on data from ~20,000 leaders in professional services. Pattern matching against a population that actually resembles the leader you’re evaluating, not a cross-industry mash-up.

Structured interview data. Used last, not first. Built around the success profile’s competencies, and used to validate and deepen what the data has already surfaced.

Any one of these instruments alone is incomplete. Doing fewer than four of these is what most PE firms do most often, but the predictive validity of the combination is materially higher than any single factor alone.

Ideally, this work runs alongside the rest of the diligence. The four-factor assessment of an executive team fits inside a standard pre-close window, produces an underwriting view and a post-close traction plan, and scales for rollups to cover the entire revenue-generating bench. Across our PE-backed professional services engagements, we’ve seen 90 percent retention of key leaders, accelerated value creation versus plan, and, in one global transformation, 21 percent margin improvement post-transition.

The result is putting hard numbers on the soft stuff. The questions PE has historically treated as judgment calls (will this person succeed, where are the gaps, how confident should we be) become measurable, predictive, and actionable. Now, rather than the output of diligence being a “yes” or “no” verdict, it’s a development plan that influences whether the leader and the leadership team actually deliver.

Doing It at Scale: Beyond the CEO and the CFO

Every PE firm wants to know they have the right CEO and CFO. And what about everyone else with a revenue target?

In professional services firms, the value creation plan doesn’t get delivered by two people at the top. It gets delivered by every partner and director who carries a number. Activate them, or the plan doesn’t land.

The shift, if you’re an operating partner, is from “do we have the right two leaders?” to “are the performance factors of our entire revenue-generating bench activated?” Same multi-factor, future-focused approach, applied to all the leaders instead of two.

And it’s not just an individual question. It’s a team question too. A roster of all-stars isn’t the same as a championship team. “Talent wins games,” as Michael Jordan put it, “but teamwork and intelligence win championships.” This matters especially in PE-backed rollups, where the typical team (long-tenured partners, acquired partners, and recent hires) has a structural composition problem that incentives alone can’t solve. Rewarding performance is nice. But leadership team effectiveness accelerates growth and creates outsized results.

From Diligence to Development: The Move Most Firms Miss

A snapshot leaves the equity owner with one decision: keep or replace the person. A multi-factor assessment shows the whole deck of cards. You see what’s in your hand, what’s missing, and what each move would cost. In reality there are three options:

- Invest in the leader you have, with a traction plan tied to business results highlighting specific performance factors and gaps.

- Complement them with a different hire structured around their gaps, rather than as a redundancy.

- Replace them.

Our experience suggests that many PE firms default to option three, even when the highest ROI might be option one or option two, and sometimes both. But you can only see that distinction if your assessment produces a development plan, not just a grade. That’s the difference between talent diligence as a pre-close box-checking exercise and talent diligence as a strategic value creation lever.

Closing Thought

Bain’s 2024 Global PE Report makes the macro case that over the last decade, roughly half of buyout returns came from revenue growth and the other half from multiple expansion, with margin expansion contributing essentially nothing, a mix Bain calls “no longer sustainable.” If the days of financial engineering as the primary value creation lever are behind us, what’s left is execution. Execution is what the right leadership teams deliver.

And yet PE hasn’t closed the loop. Bain’s separate research on talent decisions found that 80 percent of PE firms use the value creation plan to set growth targets, but only 34 percent translate those targets into clear executive role definitions. The VCP says what the company has to become. Almost no one writes down what its leaders have to become to make that happen.

The most consequential decisions deserve the most rigorous information. PE has internalized that principle for every input on a deal except one. Talent is the final frontier, still run on a map and a gut feel. The firms that will pull ahead in this cycle are the ones who do their leader’s recon and walk the ground.

I leave you with this question… is your approach to talent due diligence making the value creation plan inevitable? Or just checking the same box you’ve become accustomed to checking? If it’s the latter, we should talk. Get in touch with me directly or use the contact form on our site to start a conversation.

Nate Boaz

Nate is a Senior Partner and Co-Founder at Kinavic, where he brings a wealth of leadership performance experience from his time at McKinsey, Accenture, Microsoft, and the Marine Corps.